My Report

Integrated Report

Governance Reports

Annual corporate governance report

Managing Director/Chief Executive Officer's and Chief Financial Officer's Statement of Responsibility

Independent Assurance Report - Internal Control

Our governance framework is built on the principles of accountability, ethical conduct, and stakeholder engagement, ensuring transparency in our disclosures and decision-making.

Chairman’s Message

The rapidly evolving global landscape, characterised by digital innovation, demographic shifts, and mounting regulatory expectations, continues to redefine the banking industry. As we navigate this challenging environment, Commercial Bank remains steadfast in its commitment to upholding the highest standards of corporate governance, recognising that transparency, accountability, and ethical conduct are foundational to our long-term success and sustainability.

The year 2024 was marked by significant governance milestones. The transition of Board leadership, including my appointment as the Chairman and the reconstitution of key Board committees to align with new regulatory frameworks, underscores our dedication to maintaining a strong governance culture. These changes, coupled with the appointment of a new Director and the refinement of governance structures, have enhanced the Board’s ability to provide strategic oversight and adapt to emerging challenges.

Our governance framework is built on the principles of accountability, ethical conduct, and stakeholder engagement. At its core, this framework ensures that we not only comply with regulatory requirements but also stay true to the spirit of good governance. By fostering transparency in our disclosures and decision-making processes, we empower stakeholders and strengthen trust, which is paramount to our role as a financial intermediary.

In 2024, we continued to emphasise the integration of ESG principles into our business strategy. Our Sustainability Framework and the CSR Trust have guided our efforts to create lasting value for all stakeholders. From ethical conduct initiatives, such as the Conduct Risk Management Policy and the Anti-Bribery and Anti-Corruption Policy, to our proactive adoption of the revised Section 9 of the Listing Rules on Corporate Governance issued by the CSE, we are setting benchmarks for responsible banking in Sri Lanka.

I am pleased to affirm that the Bank has adhered to all applicable requirements of the Banking Act Directions No. 11 of 2007 issued by the CBSL and the Code of Best Practice on Corporate Governance – 2023 issued by CA Sri Lanka.

We have already taken steps to reconstitute the composition of the Board Committees of the Bank., complying with the requirements of the Banking Act Direction No. 05 of 2024 on Corporate Governance issued by the CBSL which became effective from January 01, 2025, and will take necessary steps to comply with any remaining gaps well within the stipulated timelines.

This Integrated Annual Report reflects our unwavering commitment to accountability and transparency. By exceeding mandatory disclosure requirements, we aim to provide stakeholders with a holistic view of our governance practices and sustainability initiatives. Our focus extends beyond compliance, showcasing the dedication to advancing ESG priorities and driving long-term value creation.

As we look to the future, our focus remains on delivering greater value to shareholders, fostering resilience amidst changing industry dynamics, and maintaining our reputation as a model of corporate governance. I extend my deepest gratitude to the Board, the Management team, employees, and all other stakeholders for their unwavering dedication to the Bank’s principles and goals. Together, we will continue to uphold the values that define Commercial Bank, ensuring sustainable growth and enduring success.

S Muhseen

Chairman

February 28, 2025

Colombo

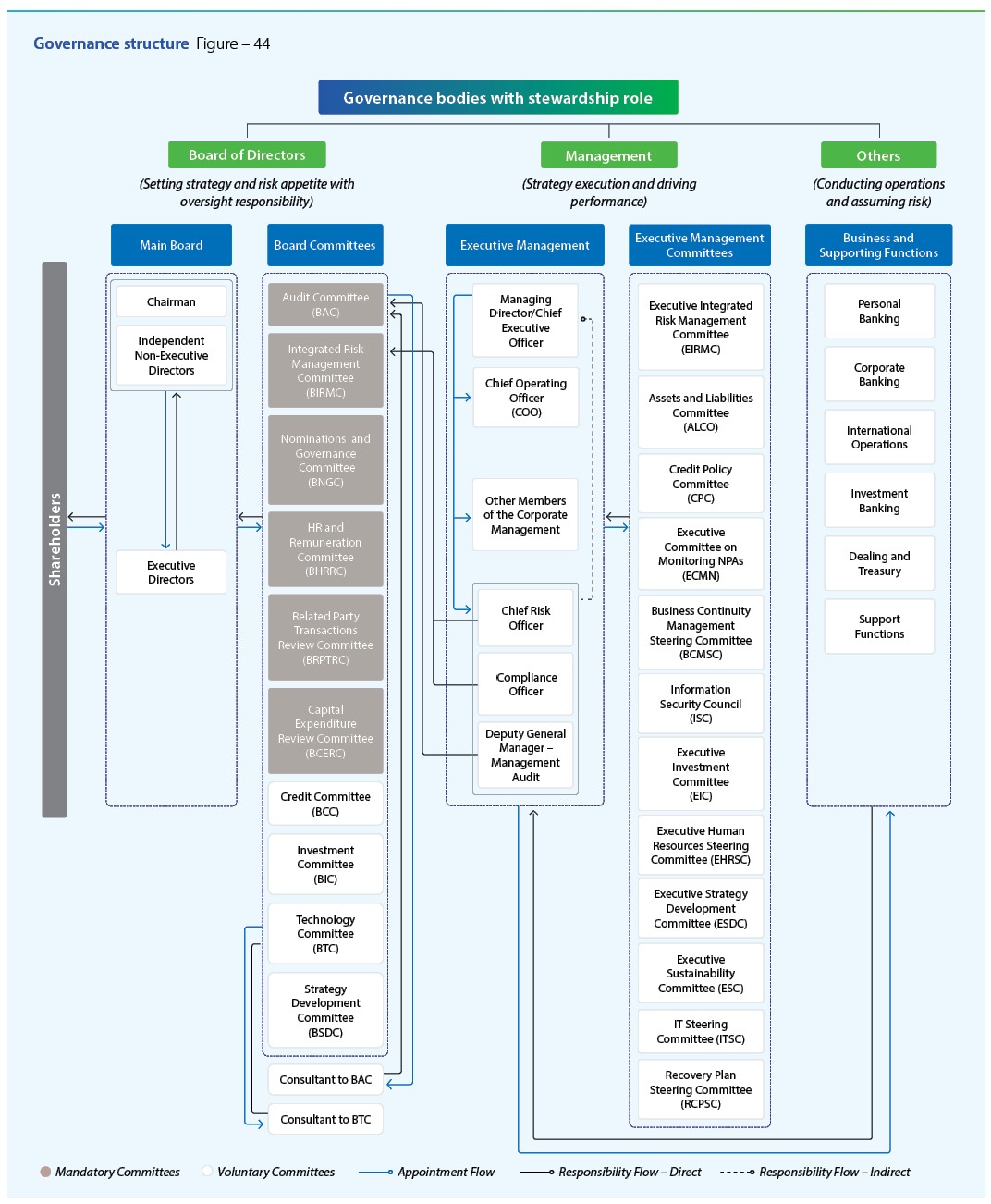

Board of Directors (Principles A.1, A.1.5, A.4, and A.10)

The Board of Directors serves as the cornerstone of governance at the Bank, embodying the principles of good corporate citizenship, ethical behaviour, transparency, and accountability. Its leadership and oversight ensure the long-term sustainability and resilience of the Bank while safeguarding its integrity and reputation.

Role and responsibilities of the Board

As the highest decision-making authority, the Board assumes a leadership role in:

- Strategic direction – Setting the strategic objectives and defining the risk appetite to ensure the Bank’s goals align with stakeholder expectations.

- Oversight and monitoring – Evaluating the Bank’s performance, overseeing compliance, and assessing internal control and risk management systems.

- Resource allocation – Ensuring the optimal utilisation of resources to deliver value.

- Corporate governance – Approving governance policies, including remuneration frameworks, and ensuring ethical business conduct.

- Appointments – Making appointments to the Board, its Committees, and Corporate Management positions.

Through diligent oversight, the Board entrusts the Corporate Management with the execution of strategies, day-to-day operations, and the implementation of robust internal control and risk management systems.

Board – Corporate Management dynamics

The Board and the Corporate Management share a clear mutual understanding of their respective roles, delegated authority, and boundaries. This relationship, grounded in trust and respect, has been instrumental in fostering good governance and organisational effectiveness. It is a hallmark of the Bank’s sustained success and its reputation as a benchmark private-sector bank in Sri Lanka.

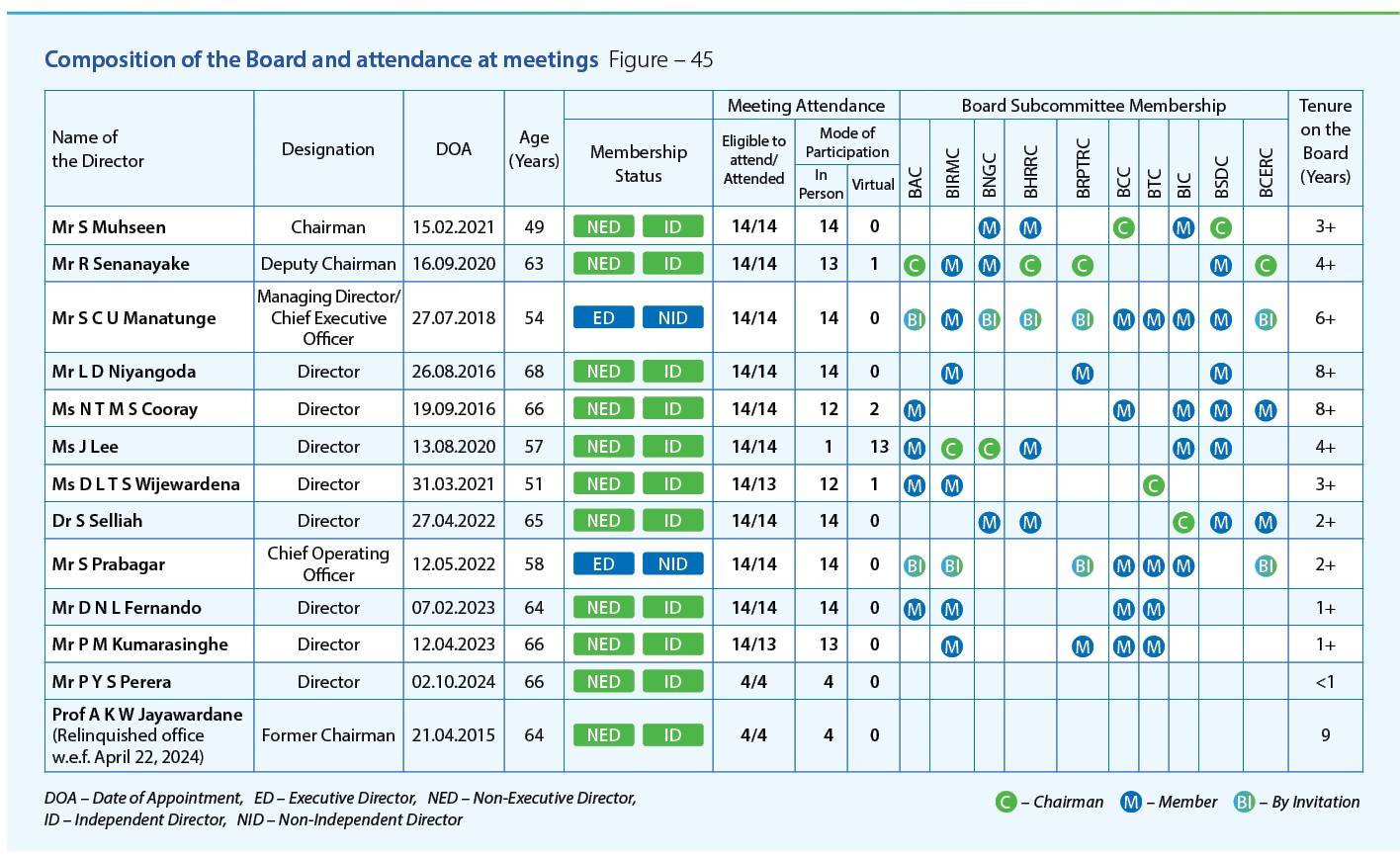

Composition of the Board

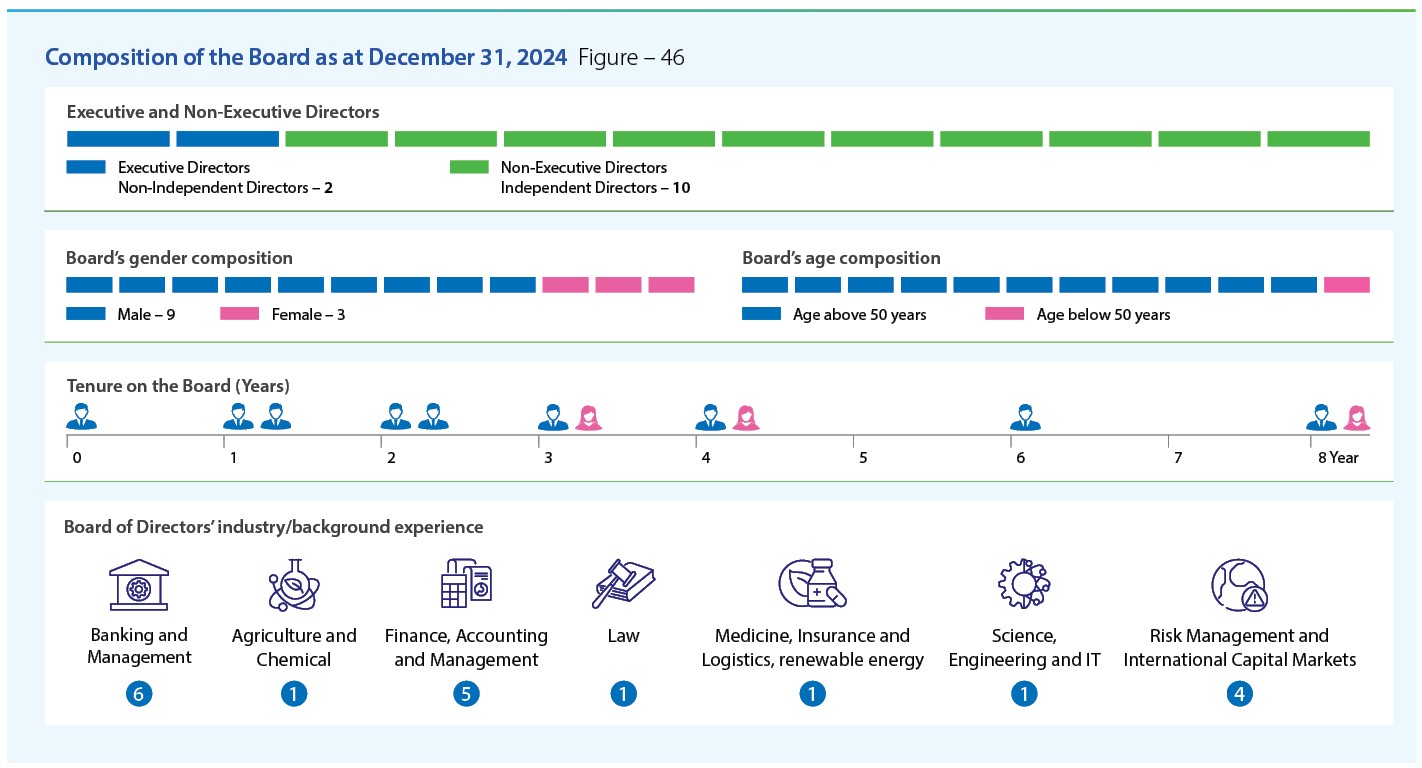

At the end of 2024, the Board comprised twelve Directors (twelve at the end of 2023 as well), including ten Independent Non-Executive Directors (INEDs), ensuring a high degree of autonomy and adherence to shareholder interests.

Each Director brings a wealth of expertise in diverse professional fields, enabling constructive challenges to the Corporate Management and enriching deliberations on complex and dynamic issues (Refer pages 38 to 45 for profiles of the Board and Figure 45 on page 199 for the composition of the Board at end of 2024.

As one of Sri Lanka’s two higher-tier D-SIBs, the Bank’s Board is acutely aware of its role in navigating emerging global challenges and threats to conventional banking models.

Diversity and inclusion

(Principle A.10.1)

Diversity and inclusion are integral to fostering a dynamic, forward-thinking organisation in the Bank. A wide array of voices and perspectives are encouraged and inclusively heard within the Bank’s working environment, driving innovation and contributing to the overall progress of the institution.

Diversity at the Board level

The Board of Directors exemplifies the Bank’s commitment to diversity by encompassing expertise across multiple disciplines, including:

- Banking and Management

- Agriculture and Chemical Industry

- Finance, Accounting and Management

- Law

- Healthcare, Insurance, Logistics and Renewable Energy

- Science, Engineering and IT

- Risk Management and International Capital Markets

Each Director has achieved significant professional milestones, having risen to leadership positions in Government institutions or private-sector organisations. Their expertise ensures that independent and informed judgment is brought to bear on matters reserved for the Board.

A unique perspective for value creation

This diversity enables the Board to:

- Blend banking, entrepreneurial, investor, and regulatory perspectives.

- Explore matters from multiple points of view to drive long-term value creation.

- Mitigate groupthink and promote healthy, constructive exchanges that enhance Boardroom dynamics and decision-making.

The Company Secretary plays a key role in supporting the Board, ensuring that he fulfills his responsibilities effectively and in line with governance principles.

Enhancing dynamics and effectiveness

The unique composition of the Board fosters an environment that values different perspectives, creating opportunities for innovative thinking and collaboration. This commitment to inclusion enhances the Board’s effectiveness in steering the Bank towards its strategic objectives.

Details on the Board’s composition, including qualifications, Committee memberships, significant appointments, and the profile of the Company Secretary, can be found on pages 38 to 45.

Board process

(Principles A.1.3, A.1.4, A.1.6, A.1.7, A.3.1, and A.6)

The Board of Directors ensures that its operations and decision-making processes are conducted with the utmost diligence, transparency, and accountability.

Maintaining transparency and accountability

- Detailed records – Minutes of all deliberations and decisions made during Board and Board Committee meetings are meticulously documented in sufficient detail, ensuring a transparent record of governance.

- Engagement with the Corporate Management – When necessary, members of Corporate Management are invited to make presentations to the Board, providing critical insights into the performance and operations of areas under their purview.

- Independent Advice – Board Members are entitled to seek independent professional advice when required, at the Bank’s expense. This ensures that Directors have access to the necessary expertise to make informed decisions.

- Liability Insurance – To safeguard Directors in the execution of their duties, the Bank has secured a Directors’ and Officers’ Liability Insurance Policy, offering protection against allegations arising from their professional responsibilities.

Access to independent expertise

Protection and support for Directors

This robust process not only facilitates effective decision-making but also ensures that governance principles are upheld at every level.

Conflicts of interest

(Principles A.5.5 and A.10.1)

The Bank has a robust system in place to identify, manage, and mitigate conflicts of interest, ensuring the integrity and independence of its Board and decision-making processes.

Declaration and management of conflicts

- Individual accountability:

- Members of the Board are required to declare any conflicts of interest or situations that could potentially lead to a conflict.

- In such cases, Directors withdraw from deliberations and refrain from influencing decisions where the conflict exists or may appear to exist.

- All such declarations and actions are minuted for future reference.

- Regular reviews:

- Affiliations and transactions of Directors are periodically reviewed to ensure that there are no conflicts of interest or relationships that could compromise their independence.

Related Party Transactions Policy

The Board has implemented a Related Party Transactions Policy, which outlines procedures for granting accommodations to Directors, their close family members, and entities in which the Directors hold directorships. These transactions are conducted in compliance with the CBSL rules and regulations, under terms and conditions applicable to other customers of the Bank.

Approval and oversight of Related Party Transactions

- Approval process:

- Related party transactions are first reviewed and recommended by the BCC.

- Final approval is granted by the Board.

- Reporting to Committees:

- Once approved, such transactions are tabled at the next scheduled meeting of the BRPTRC for information.

- Disclosure:

- The section on ‘Directors’ Interest in Contracts with the Bank’ (pages 252 and 253) provides details of transactions conducted on an arm’s-length basis with entities associated with the Bank’s Chairman or Directors.

- Further details can be found under “Related Party Disclosures” in Note 62 to the Financial Statements (pages 420 to 424).

- Quarterly declarations:

- At the time of joining and every quarter thereafter, Directors are required to declare their interests. This ensures the continuous monitoring of any potential conflicts.

- Register of interests:

- A register of declared interests is maintained by the Company Secretary, ensuring transparency and compliance with the Companies Act No. 07 of 2007 and amendments thereto

- This register is available for inspection by shareholders or their authorised representatives as per legal requirements.

Ongoing declarations and registers

This comprehensive system ensures that the Bank’s governance processes remain transparent, ethical, and free from conflicts of interest, reinforcing stakeholder confidence.

Board meetings

(Principles A.1.1 and A.10.1)

In 2024, the Board of Directors of the Bank convened fourteen scheduled meetings, maintaining the same number as in 2023. These meetings served as a vital platform for overseeing the Bank's strategic, financial, and operational performance.

Key focus areas of Board deliberations

- Strategic planning:

- One meeting was specifically allocated to reviewing the Corporate Plan 2025–2029 and Budget 2025, with active participation from the Corporate Management.

- The Board provided directions for preparing the Bank's five-year strategic plan, critically evaluating proposals and exploring alternative strategies before approving the resource allocation.

- Performance and risk review:

- Financial and operating results against budgeted KPIs and prior periods.

- Risk factors impacting results and mitigation measures.

- Monitoring the progress of the restructuring process of the foreign currency denominated Sri Lanka Government Debt and its impact on the Bank’s investments.

- Compliance with mandatory and voluntary requirements, addressing corrective actions for non-compliance.

- Updates on credit quality, including the staging of non-performing credit facilities and recovery actions.

- ESG risks and opportunities, alongside discussions on wider sustainability objectives.

- Cybersecurity risks, mitigation strategies, and compliance reports, particularly for critical systems.

- Governance and oversight:

- Review of internal control lapses, fraud investigations, and follow up actions.

- Regular updates on strategy implementation and investment strategies.

- Minutes of Board Committee meetings to ensure alignment and oversight.

- Share transactions by employees at Assistant Manager grade and above.

- Review and approval of updated policies and procedures to align with new CBSL directions.

- Capital and liquidity management:

- Emphasis on enhancing provision coverage, optimising liquidity and capital management, and addressing the rising tax burden to support stability and sustainable growth.

- Subsidiary oversight:

- Periodic presentations by the Managing Directors/Chief Executive Officers of subsidiaries on their performance and future plans.

Twelve meetings were devoted to reviewing:

Reorganisation post-AGM

Following the Fifty-Fifth Annual General Meeting (AGM) held on March 28, 2024, the Board conducted a meeting to review and revise the composition of its Committees.

Attendance and hybrid meeting format

The Bank continued to adopt a hybrid approach to Board meetings, seamlessly integrating virtual participation for Directors residing or traveling overseas or those encountering unavoidable circumstances. This inclusive approach ensured uninterrupted collaboration, enhanced engagement, and effective decision-making, while upholding the Bank’s commitment to governance excellence.

Regulatory compliance and policy updates

In response to CBSL Directions Nos. 13 and 14 of 2021, which required revisions to the classification and measurement of financial assets and credit facilities, the Board reviewed and approved necessary updates to ensure compliance with regulatory standards.

Enhancing governance and value creation

The Board’s focus extended to liquidity and capital management, ensuring resilience and stability, regular evaluation of ESG and cybersecurity risks and monitoring distressed credit facilities and resolving exposures to high-risk industries.

Board committees

(Principles A.7.1 to A.7.3, A.7.5 & A.7.6, B.2, D.3 to D.5)

The Bank has established ten Board Committees, each entrusted with delegated authority to enhance governance and address subject-specific and specialised matters. These Committees play a vital role in the Bank’s governance framework, enabling the Board to focus on broader strategic issues while ensuring that specialised areas receive the necessary attention.

Mandatory and voluntary committees

- Mandatory Board Committees:

- The Banking Act Directions No. 05 of 2024 on Corporate Governance mandates licensed banks to establish five mandatory committees, including the BRPTRC, effective from January 01, 2025. However, the Bank had voluntarily established BRPTRC in 2014, aligning with the early adoption of the Code of Best Practice on Related Party Transactions issued by the SEC, which later became mandatory.

- The Banking Act Directions No. 01 of BCERC to address restrictions on discretionary payments.

- Voluntary Board Committees:

- The remaining four Committees were formed based on the Bank’s business, operational, IT, and strategic needs, as permitted under its Articles of Association.

- These Committees underscore the Bank’s commitment to good governance and operational excellence.

- Committee operations – Each Committee meets regularly, with a minimum of one meeting per quarter.

- Use of external expertise – Committees have sought guidance and advice from external consultants as needed.

- Director participation – Each Director served on at least three Committees during the year, ensuring broad oversight and engagement.

- The Board retains overall responsibility for decisions made by the Committees, ensuring alignment with the Bank’s governance framework.

- Matters arising from Committee meetings are regularly deliberated at Board meetings for information or approval, with any specialised concerns referred back to the Committees for further oversight.

- Minutes of Committee meetings are carefully recorded, capturing Directors’ views and deliberations on key issues.

Governance and functionality

Accountability to the Board

Key reports and details

Comprehensive details on the composition of each Committee, their areas of responsibility, key activities during 2024, and attendance records of members are given in the Board Committee Reports on pages 214 to 237 of this Report.

Shareholder engagement and voting (Principles C.1, C.2, E, and F)

The Bank maintains a robust framework for engaging with shareholders, prioritising transparency, equitable treatment, and the facilitation of shareholder rights. These efforts are aligned with good corporate governance practices and a commitment to open communication.

Shareholder communication

- Board-approved Shareholder Communication Policy ensures timely and effective dissemination of material information.

- Communication methods include:

- Dividend declaration for 2023.

- Annual and interim financial statements.

- Fitch Ratings preview.

- Appointments and retirements of Directors.

- Listing of shares issued as part of the 2023 final dividend, rights issue and ESOPs.

- Basel III-compliant convertible debenture issue details.

- The dedicated “Investor Relations” page provides easy access to financial statements, annual reports, and investor feedback features.

Regulatory compliance

Encouraging shareholder participation

- Clear instructions on voting procedures are circulated with meeting notices.

- Shareholders vote on re-elections, financial statements adoption, and other key matters.

- 158 Voting and 76 Non-Voting shareholders attended in person.

- 99 Voting and 24 Non-Voting shareholders voted via proxy.

- EGMs:

- Approval was secured in March 2024 for issuing Basel III-compliant convertible debentures to raise Rs. 20 Bn., in Tier II capital to improve capital adequacy and to support future lending growth.

- Approval was secured in July 2024 for making a rights issue of shares to raise Rs. 22.5 Bn., in Tier I capital to improve capital adequacy.

Commitment to equity and rights

The Board ensures all shareholders are treated equitably, their rights are protected, and they are encouraged to actively participate in governance processes.

A detailed tabulation of AGM attendance over the past five years is provided below:

Attendance at AGMs held during the period 2020 – 2024 Table – 46

-DP_Edited-web-resources/image/213.png)

Voting shareholders |

Non-voting shareholders |

|||||

| Year of the AGM | Number of Attendees |

Shareholding | % of total shareholding |

Number of Attendees |

Shareholding | % of total shareholding |

| 2024 | 257 | 975,632,759 | 78.89 | 100 | 8,534,514 | 10.99 |

| 2023 | 301 | 943,963,856 | 80.87 | 112 | 10,962,985 | 15.11 |

| 2022 | 183 | 795,203,283 | 72.33 | 9 | 4,197,212 | 6.17 |

| 2021 | 169 | 795,052,531 | 72.32 | 19 | 4,326,942 | 6.36 |

| 2020 | 119 | 672,118,061 | 69.92 | 19 | 3,132,256 | 4.72 |

Attendance at AGMs Graph – 47

Code of Business Conduct and Ethics (Principle D.6)

The Bank maintains a robust Code of Ethics that governs the conduct of all employees, including KMPs. This Code, complemented by other Board-approved policies, ensures that the Bank adheres to the highest standards of integrity, transparency, and accountability.

Scope of the Code of Ethics

- Employee coverage – Currently applicable to all employees, including KMPs.

- Board of Directors coverage – The Bank extended application of the Code of Ethics to include the Board of Directors in 2024, through the Board-approved Policy on Internal Code of Business Conduct and Ethics.

- Transparency – Encouraging open communication and disclosure.

- Accountability – Holding all employees accountable for their actions.

- Integrity – Promoting honesty and fair dealings in all professional interactions.

- Conflict of Interest – Providing clear guidelines to avoid and manage conflicts of interest.

- Compliance – Adhering to all legal and regulatory requirements.

Alignment with Governance Principles

(Principles D.6.1 to D.6.6)

The Code addresses key topics to ensure compliance with the principles of ethical behaviour, including:

The Bank’s Code of Business Conduct and Ethics serves as a cornerstone for maintaining trust among stakeholders, ensuring the alignment of actions with the Bank’s values and principles.

Alignment with Governance Principles Table – 47

| Topic | Key policies, documents and guidelines | |

| Conflict of interest |

|

|

| Bribery and corruption |

|

|

| Entertainment and gifts |

|

|

| Accurate accounting and record-keeping |

|

|

| Fair and transparent procurement policies |

|

|

| Corporate opportunities |

|

|

| Confidentiality |

|

|

| Fair dealing |

|

|

| Protection and proper use of company assets including information assets |

|

|

| Sexual harassment, discrimination and abuse |

|

|

| Compliance with laws, rules and regulations (including insider trading laws) |

|

|

| Encouraging the reporting of any illegal, fraudulent or unethical behaviour |

|

Principle D.6.2

Process is in place to identify and report material and price sensitive information.

Principle D.6.3

Process is in place to monitor and disclose shares purchased by any Director, KMP or by an employee in the grade of Assistant Manager and above

Principle D.6.4

Whistleblower’s charter

Principle D.6.5

Conduct training on Code of Ethics as part of induction and training of new employees

Principle D.6.6

Process is in place to disseminate policies and conduct training via the Bank’s intranet and the e-learning module

Anti-Bribery and Anti-Corruption Policy

(Principle D.6.1)

The Bank upholds a zero-tolerance policy towards bribery and corruption, ensuring that all operations and transactions are conducted with the highest standards of integrity and compliance.

Policy framework

- Annual review and updates:

- The Board-approved Anti-Bribery and Anti-Corruption Policy was reviewed and updated during the year.

- The Policy outlines principles for identifying, mitigating, and managing bribery and corruption risks, applying to the Bank, its employees, and defined third parties.

- Zero tolerance commitment:

- The Bank treats any form of bribery or corruption as a severe threat to its integrity and reputation.

- Employees are expected to actively prevent and mitigate risks within their respective roles and responsibilities.

- Code of Ethics:

- Every employee is issued a Code of Ethics, which includes:

- Prevention of insider trading and

rules on the purchase or sale of the Bank’s shares. - Gift Policy guidelines.

- Management of conflicts of interest.

- Measures to combat financial crimes.

- Emphasis on respecting communities and the environment.

- Prohibition of political contributions:

- The updated Policy explicitly prohibits the use of Bank funds for political contributions, emphasising the Bank’s stance on neutrality and compliance.

Employee responsibilities and guidelines

Culture of compliance

The Policy is designed to promote a culture of compliance aligned with applicable laws and regulations, ensuring that ethical practices remain a cornerstone of the Bank’s operations.

Further insights on the Bank’s sustainable practices in line with this Policy are discussed in the section on Responsible organisation on pages 129 and 130.

Group Conduct Risk Management Policy Framework

(Principle D.6.1)

The Group Conduct Risk Management Policy Framework of the Bank emphasises a proactive approach to mitigating misconduct risks, fostering accountability, and promoting ethical practices across all operations.

Policy updates and enhancements

- Originally adopted in 2022, the framework was reviewed and updated during the year to further strengthen risk management and corporate governance.

- The updated policy focuses on safeguarding customers, maintaining market stability, and ensuring effective competition.

- Establishing a risk culture:

- Cultivating a preventive approach to misconduct risks.

- Promoting accountability for individual and collective actions.

- Preventing misconduct:

- Ensuring proper customer onboarding practices.

- Maintaining transparency in fees and charges.

- Prohibited actions:

- Fraudulent activities

- Insider trading

- Improper financial advice to customers

- Mis-selling of financial products

- Tax avoidance

- Collusion in financial markets

- Inaccurate financial and regulatory disclosures

- Oversight by the Compliance Officer:

- The Compliance Officer is designated to manage the whistleblowing process, ensuring proper handling of all concerns raised.

- Encouraging reporting of concerns:

- Employees are encouraged to raise genuine concerns about malpractices or unethical behaviour.

- Confidentiality and protection:

- The Bank ensures strict confidentiality for individuals who report concerns.

- Whistleblowers acting in good faith are protected from any retaliation or adverse consequences.

- Promoting governance across tiers:

- The charter promotes a healthy workplace culture, fostering good governance practices from operational levels to the highest tiers of management.

Key objectives

This Policy underpins the Bank’s commitment to ethical conduct and operational excellence, aligning with its broader risk management framework and corporate governance principles.

Whistleblowing

(Principle D.6.4)

The Whistleblowers’ Charter adopted by the Bank serves as a crucial tool in deterring, detecting, and addressing malpractices and unethical behaviour across the organisation.

Key features of the whistleblowers’ charter

Internet of things and Cyber security

(Principle G)

The Bank prioritises robust cybersecurity measures and effective governance to ensure data confidentiality, integrity, and availability in an increasingly connected and digital environment.

Fortifying digital trust: cyber and information security governance

In an era where financial institutions are increasingly reliant on technology, the Bank remains steadfast in its commitment to safeguarding digital platforms, protecting data integrity, and preserving customer trust. Recognising the ever-evolving cyber threat landscape, the Bank takes a proactive approach to cybersecurity, ensuring compliance, resilience, and operational continuity. As a D-SIB, the Bank also plays a pivotal role in strengthening Sri Lanka’s cyber-resilient financial ecosystem.

Industry leadership in cybersecurity and compliance

The Bank has cemented its position as a leader in information security, achieving several industry-first certifications that underscore its dedication to best practices:

- ISO/IEC 27001:2022 Certification – The only local financial institution in Sri Lanka to secure this latest certification, covering its entire operation, including its nationwide branch network.

- PCI DSS v4.0 Certification – Ensuring the highest security standards in handling payment card transactions.

- ISO/IEC 20000 Certification – Validating excellence in IT service management.

- Alignment with ISO/IEC 22301:2019 – Strengthening Business Continuity Management Systems (BCMS) to enhance resilience and preparedness.

These milestones reaffirm the Bank’s longstanding legacy in cybersecurity, dating back to 2010 when it became the first in Sri Lanka’s banking sector to achieve ISO 27001 certification.

A strong governance framework for information security

The Bank has embedded cybersecurity governance within its enterprise risk management framework, ensuring robust oversight through a three lines model. This approach integrates business units and technology teams responsible for implementing security controls, independent risk and audit functions that provide monitoring and assessments, and Board-level oversight to ensure accountability.

At the core of the Bank’s information security governance is the Chief Information Security Officer (CISO), who reports directly to the MD/CEO. The Information Security Council (ISC), chaired by the MD/CEO, functions as the apex management body for cybersecurity and reports to the BIRMC. The Bank’s Information Security Policy (ISP), aligned with ISO/IEC 27001 standards, defines stringent security requirements applicable to employees, partners, and external stakeholders. These policies encompass essential domains such as access control, asset management, secure operations, incident response, supplier and third-party risk management, and business continuity planning.

A multi-layered security architecture with a proactive risk management approach

To ensure comprehensive protection of its digital assets, the Bank employs a defense-in-depth security model that integrates multiple layers of physical, technical, and administrative controls. A Security Information and Event Management (SIEM) system enables real-time monitoring and rapid threat detection, while a set of incident response playbooks and cyber resilience strategies enhance the Bank’s ability to contain and mitigate potential cyber threats.

Regular risk assessments, including vulnerability testing, penetration testing, and application security reviews, help identify and address security risks. In 2024, the Bank further strengthened its third-party security risk management processes, ensuring enhanced oversight of supplier and partner cybersecurity practices.

Building a cybersecurity-first culture

Beyond deploying advanced technologies, the Bank recognises that security is also a matter of culture and awareness. A structured cybersecurity awareness program ensures that employees and third parties are well-equipped to recognise and respond to cyber threats. Training programs include classroom sessions, digital learning modules, and hands-on simulations of potential cyberattacks. The annual Cyber Awareness Month serves as an engaging initiative, featuring interactive activities such as cyber quizzes and newsletters that reinforce best practices across all levels of the organisation.

Rigorous monitoring, audits, and regulatory compliance

The Bank maintains continuous compliance through an extensive framework of internal and external audits. Annual independent validations of the Information Security Management System (ISMS) are conducted by ISO 27001 external auditors, while Qualified Security Assessors (QSA) perform periodic reviews to ensure compliance with PCI DSS requirements. The Bank’s adherence to the SWIFT Customer Security Controls Framework is independently verified, reinforcing its commitment to international cybersecurity standards. Regular reviews of cybersecurity performance, including incident reports and audit findings, are presented to the ISC and BIRMC, ensuring Board-level engagement and strategic oversight.

A future-ready cybersecurity roadmap

As cyber threats continue to evolve, the Bank remains committed to staying ahead of emerging risks through investments in AI-driven threat detection, Zero-Trust security models, and enhanced cyber resilience frameworks. Strengthening security infrastructure and continuously aligning with global best practices remain central to the Bank’s long-term vision.

For in-depth discussions on the Bank’s cybersecurity governance, refer to:

- BIRMC Report

- BTC Report

- BAC Report

With an unwavering commitment to cybersecurity, resilience, and trust, the Bank continues to set the benchmark for information security excellence in Sri Lanka’s banking industry.

Data security and privacy

The Bank is committed to safeguarding the privacy and security of customers' personal data through rigorous data governance practices. The Bank ensures compliance with evolving regulatory frameworks, including the Personal Data Protection Act No. 09 of 2022, while continuously strengthening data protection measures to maintain customer trust.

Commitment to data privacy

Protecting the confidentiality, integrity, and availability of personal data is at the core of the Bank’s operations. A robust framework encompassing skilled personnel, advanced technology, stringent controls, well-defined policies, and efficient processes ensures responsible management of personal data. All customer information is handled with the highest level of security and is used exclusively for legitimate business purposes in compliance with applicable privacy laws and regulations, including the Personal Data Protection Act and Global Data Protection Regulation (GDPR).

Privacy framework and third-party collaborations

The Bank has established a comprehensive privacy framework to safeguard customer information. Stringent data privacy and security standards are enforced when collaborating with third-party service providers. Due diligence assessments, contractual safeguards, and continuous monitoring ensure that personal data remains protected across all external engagements.

Employee training and awareness

Recognising that data privacy is a shared responsibility, the Bank conducts regular training and awareness programs to educate employees on data protection best practices. These sessions equip staff with the knowledge to handle personal data securely, stay informed of evolving privacy regulations, and uphold the highest standards of data security.

Governance and Risk Management

The data governance team plays a pivotal role in identifying, assessing, and mitigating data privacy risks. These risks are regularly reported at the highest levels of management, ensuring a proactive approach to data protection. Data privacy is a key focus at multiple governance forums, including Board-level discussions, to facilitate strategic oversight and timely decision-making.

As part of its commitment to continuous improvement, the Bank regularly reviews and enhances its data privacy practices to stay ahead of emerging threats, evolving technologies, and regulatory changes. Protecting personal data remains a top priority as the Bank continues to build a secure and trustworthy financial ecosystem for its customers.

Sustainability: ESG risks and opportunities

(Principle H)

The Bank recognises that integrating ESG principles into its strategy and operations not only aligns with global sustainability goals but also enhances innovation, risk mitigation, and long-term value creation.

Integration of ESG principles

- Strategic focus:

- The Bank integrates ESG principles into decision-making processes to mitigate risks and capitalise on emerging opportunities.

- Compliance with relevant regulations and adaptation to evolving stakeholder needs form a cornerstone of the Bank’s ESG strategy.

- Measurement and disclosure:

- Utilises globally recognised frameworks such as the GRI standards and the <IR> Framework.

- Regularly measures and discloses sustainability performance to foster transparency and accountability.

- Sustainability Framework:

- Adoption of a comprehensive framework and establishment of an Executive Sustainability Committee, which reports to BIRMC, for regular ESG risk assessments.

- ESMS:

- Based on IFC Performance Standards, ESMS includes policies and tools for managing environmental and social risks.

- Due diligence and impact assessment:

- Conducts environmental and social due diligence and proposes corrective actions for identified risks.

- Evaluates the impact of lending activities on factors such as pollution, community well-being, and biodiversity.

- Responsible lending practices:

- Maintains a credit policy and lending guidelines to minimise transactions that adversely impact the environment.

- Supply chain oversight:

- Reviews social and environmental impacts through supplier selection and evaluation.

- Minimising environmental footprint:

- Implements green processes, adopts green buildings, and generates solar energy for operations.

-DP_Edited-web-resources/image/276.png) Green financing:

Green financing:- Supports sustainable projects such as renewable energy, energy-efficient buildings, and eco-friendly technologies.

- Encourages clients to adopt sustainable practices through green loans and leases.

- Supplier collaboration:

- Works with responsible suppliers to minimise indirect environmental and social footprints.

- Staff training and engagement:

- Conducts training programmes to enhance staff understanding of sustainable finance and ESG principles.

- International partnerships:

- Actively collaborates with global platforms to share knowledge and leverage international resources for

ESG initiatives.

ESG risk management initiatives

Leveraging ESG opportunities

The Bank’s ESG strategy reflects its commitment to sustainable value creation, proactive risk management, and global

best practices.

1 Principles referred to in this section are the principles in the Code of Best Practice on Corporate Governance – 2023 issued by CA Sri Lanka.