My Report

Integrated Report

Risk governance and management

Managing Director/Chief Executive Officer's and Chief Financial Officer's Statement of Responsibility

Independent Assurance Report - Internal Control

Navigating risks in a recovering economy

The year 2024 marked a pivotal turning point for Sri Lanka’s economy, as the country made significant strides in its post-crisis recovery. After the severe economic and foreign exchange crisis of 2022, the country's reforms, supported by the USD2.9 Bn. IMF program, started to show positive outcomes. Real GDP expanded by 5.2% in the first 9 months of 2024, the highest growth rate in 5 years, signaling renewed stability and confidence. Additionally, the successful completion of Sri Lanka’s debt restructuring in December 2024 further strengthened its fiscal position, laying a foundation for long-term economic resilience. Notably, these achievements were realised despite the political uncertainties of holding two key elections, underscoring growing institutional stability and policy continuity.

Amidst these developments, monetary policy played a crucial role in balancing growth with stability. To support economic expansion, the Central Bank of Sri Lanka (CBSL) gradually reduced the Standing Deposit Facility Rate (SDFR) and the Standing Lending Facility Rate (SLFR) from 9% and 10% at the beginning of the year to 8.25% and 9.25% respectively by October 2024. In November, CBSL introduced a unified Overnight Policy Rate (OPR) at 8%, marking a key shift towards a simplified monetary policy framework. Combined with easing energy prices and administrative interventions, these measures anchored inflation at a medium-term target of 5%, with the Colombo Consumer Price Index (CCPI) recording a year-on-year deflation of 1.70% in December 2024.

Despite these positive developments, challenges persist. The IMF has emphasised the importance of fiscal prudence, particularly in achieving tax revenue targets and reforming state-owned enterprises, as the country works towards a primary surplus target of 2.3% of GDP in 2025. Structural vulnerabilities in Sri Lanka’s economy necessitate sustained policy discipline and continued reforms. Additionally, global economic uncertainties and potential commodity price fluctuations demand careful monitoring of the economic environment.

For the banking sector, these dynamics create a complex risk landscape. While economic recovery presents new opportunities, potential volatility in inflation, interest rates, and fiscal policy decisions necessitates proactive risk management. The Bank continued to strengthen its risk frameworks, with a heightened focus on stress-testing, scenario analysis, capital adequacy and internal measures ensuring regulatory compliance. Robust credit risk management remains critical as businesses and individuals adjust to evolving economic conditions. Furthermore, ongoing investments in digital transformation, operational resilience and skill development are vital to navigating an increasingly sophisticated risk landscape.

As the economy transitions from crisis to recovery, a prudent and forward-looking approach to risk management is more important than ever. The Bank remains committed to safeguarding its financial soundness while supporting the country’s economic revival. By staying agile and adaptive in a rapidly evolving landscape, the Bank will continue to manage risks effectively, ensuring sustainable growth and stability for all stakeholders.

Balancing growth and risk

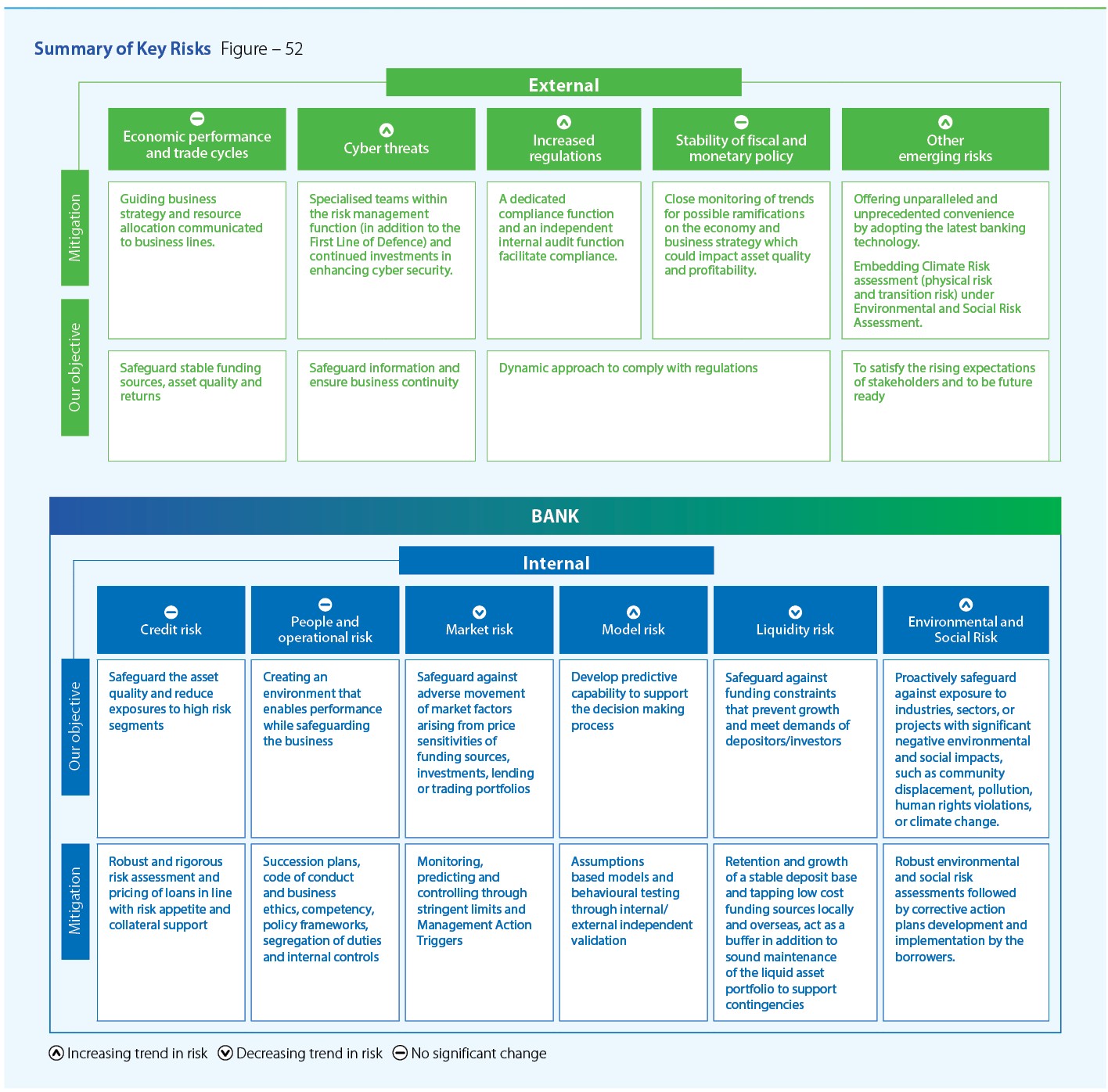

As a leading financial institution, the Bank's operations center on financial intermediation and maturity transformation (refer to the Business Model for Sustainable Value Creation). As of December 31, 2024, the Bank managed an on-balance sheet asset base of Rs. 2,789.78 Bn., leveraging a capital base of Rs. 285.63 Bn., 9.8 times. While this leverage facilitates growth, it necessitates vigilant management of key risks – credit, operational, and market risks – aligned with Basel capital adequacy standards.

Beyond these core risks, emerging challenges such as digital disruptions, geopolitical volatility, and evolving regulatory frameworks introduce additional complexities. These external uncertainties, coupled with sector-specific risks, have the potential to influence all risk categories.

The Bank’s robust risk governance framework and proactive management strategies ensure a well-calibrated balance between risk and return. By continuously refining risk mitigation techniques, the Bank safeguards stakeholder confidence particularly among depositors and upholds its commitment to sustainable value creation.

Advancing risk management

As the authority for designing, calibrating, and deploying risk rating models, Integrated Risk Management Department (IRMD) has bolstered the Bank's compliance with regulatory requirements and enhanced the acceptability of these models. To ensure the robustness of credit risk evaluation frameworks for its lending operations, the IRMD has implemented external validation processes, covering all credit risk assessment models, subject to periodic review.

To extend its expertise beyond the core banking operations, IRMD has collaborated with Bank’s financial subsidiaries as well as Bangladesh operations to implement best practices in managing credit, operational, market, and environmental risks across the Group.

The introduction of Data Governance and Business Intelligence Unit marks another milestone, enabling enhanced regulatory compliance and robust internal data protection measures. With a view to enhance operational efficiency and to significantly reduce turnaround times in the SME lending, IRMD collaborated with the internal stakeholder units to recalibrate SME credit scoring models.

Looking ahead, IRMD’s strategic focus includes digital transformation initiatives such as implementing a Data Repository and Data Marts. Further, the Department has outlined a five-year plan to integrate Environmental, Social, and Climate Risk (ESCR) considerations into the Bank’s Risk Management Framework. This plan aims to align climate risk governance, scoring, and data-driven disclosures with the Bank’s sustainability goals, ensuring resilience, regulatory compliance, and sustainable growth.

By embedding sound risk management practices and leveraging technological advancements, IRMD continues to play a pivotal role in driving the Bank’s strategic objectives and ensuring long-term value creation.

Key objectives of risk oversight

The key objectives of the Bank’s risk governance framework and risk management function are designed to ensure resilience, stability, and sustainable growth. These objectives include:

- Building a robust risk management structure: Establishing a well-defined organisational framework for effective risk oversight and management across all levels of the Bank.

- Defining and aligning risk appetite: Articulating the desired risk profile, encompassing risk appetite and tolerance thresholds, to align with the Bank's strategic objectives.

- Fostering a positive risk culture: Promoting a culture where values, beliefs, and practices encourage proactive risk awareness and informed decision-making.

- Assigning responsibility and accountability: Clearly defining responsibilities for accepting, mitigating, transferring, or minimising risks, with a focus on recommending optimal approaches.

- Ongoing risk profiling: Continuously monitoring and evaluating the Bank’s risk profile against approved risk appetite to maintain alignment with strategic goals.

- Quantifying potential losses: Identifying plausible risk exposures and estimating potential financial and operational impacts.

- Conducting stress-testing: Regularly performing stress tests to ensure the Bank maintains sufficient capital and liquidity buffers to absorb shocks and meet obligations.

- Leveraging technology in risk management: Adopting advanced analytics and digital tools to enhance risk assessment, monitoring, and reporting.

- Integrating risk with strategy: Embedding risk considerations into the formulation and execution of business strategies to align operational decisions with risk objectives.

- Optimising capital utilisation:Ensuring that capital is effectively deployed to achieve an optimal balance between

risk and return. - Enhancing risk communication: Strengthening communication channels to ensure a shared understanding of risks across all organisational levels.

- Promoting stakeholder trust: Demonstrating robust risk governance to maintain confidence among stakeholders, including investors, customers, and regulators.

Key challenges to risk oversight in 2024

- Challenges in addressing Environmental, Social, and Governance (ESG) risks and Climate Risk assessment: The increasing global and local focus on ESG factors presents significant challenges for the banking sector. Sri Lankan banks face hurdles in developing and integrating robust climate risk assessment frameworks, as these frameworks are still in their infancy. The absence of established benchmarks and the need for significant investments in tools, expertise, and systems further compound these challenges.

- Aligning with global ESG standards and opportunities in sustainable finance: Simultaneously, heightened regulatory expectations for ESG compliance drive the need for structured climate finance strategies. The Bank is proactively aligning with SLFRS S1 & S2 reporting standards, expanding its green finance portfolio, and developing sustainability-linked credit products. Key initiatives include implementing a Climate Risk Assessment Framework, developing a Climate Transition Plan, conducting stress-testing for ESG factors, and fostering stakeholder engagement. By embedding ESG principles into core lending and investment decisions, the Bank aims to mitigate regulatory and reputational risks while positioning itself as a leader in sustainable finance.

- Climate risk integration in credit and stress-testing: Given Sri Lanka’s vulnerability to natural disasters, integrating climate risk into credit evaluation processes and stress-testing is becoming a priority. The Bank is planning to commence climate-related stress-testing in 2026, which will involve assessing the potential financial impacts of extreme weather events on borrowers and the portfolio. This integration requires the development of robust methodologies, access to reliable environmental data, and training for risk management professionals to interpret climate-related risks effectively.

- Infrastructure and expertise gaps in digitisation: While the banking industry is accelerating its digital transformation, gaps in digital infrastructure, limited expertise, and slow adoption rates present significant challenges. Collaborative efforts with the Bank’s Data Science Team of the IT Research & Development Unit and external consultants are crucial to bridge these gaps. This journey highlights the need for continuous skill development within the IRMD as well as among the stakeholder departments and units and alignment across departments to achieve meaningful digital transformation.

- Heightened regulatory requirements: Stricter regulatory requirements regarding compliance, corporate governance, capital adequacy, liquidity management, and sustainability are expected to intensify over the next 2–3 years. Banks will be required to allocate substantial resources to meet these evolving demands. This includes implementing governance and risk frameworks that align with both local and international regulations. Adhering to these requirements while managing costs and operational efficiency will be a significant balancing act for the Bank.

- Cybersecurity risks and data protection: The banking sector faces an escalating threat from cyberattacks and data breaches, necessitating continuous investments in robust cybersecurity frameworks. The Bank prioritises the protection of customer and institutional data through multi-layered security measures. Proactive cybersecurity initiatives include periodic vulnerability assessments/penetration testing, independent security assessments, and ongoing employee training to reinforce cyber hygiene practices. The Bank also ensures strict adherence to CBSL directives and global cybersecurity standards, including ISO/IEC 27001 and Payment Card Industry Data Security Standards (PCI DSS), further strengthening its resilience against evolving cyber threats.

- Talent acquisition and retention challenges: The demand for skilled risk professionals with up-to-date knowledge in relevant technologies is growing, both locally and globally. Attracting and retaining such talent is becoming increasingly challenging owing to scarcity, especially as specialised skills like ESG risk analysis, cybersecurity, and data analytics. The Bank is on a journey of nurturing internal talent while positioning itself as a preferred employer to attract external expertise.

- Rising operational costs and efficiency pressures: The transformation of legacy risk management processes into digital formats is already underway with the collaborative support of stakeholder units as well as through the services of external consultants. However, optimising resource allocation, leveraging automation, and ensuring cost efficiency remain ongoing challenges.

- Technological obsolescence: Rapid advancements in technology demand continuous upgrades to systems and processes. Falling behind on technological adoption could affect operational resilience and the ability to compete in an increasingly digitalised banking landscape.

Key risk management initiatives adopted in 2024

- Digital transformation in risk management: The IRMD has taken significant strides in digitizing risk management processes. Initiating the implementation of a Risk Data Repository and Data Marts, the Department is on a transformative journey. These initiatives aim to streamline risk management activities, enhance internal governance, and drive greater operational efficiency, consistency and alignment across departments.

- Integration of environmental and social risks: Recognising the importance of environmental and social factors, the Bank has incorporated these risks into its Internal Capital Adequacy Assessment Process (ICAAP). This enhancement enables improved evaluations of potential impacts through internally developed stress-testing methodologies.

- Enhanced application of Risk Adjusted Return on Capital (RAROC): Strengthening credit risk evaluation, the Bank has externally validated its RAROC assessment methodologies and processes, ensuring adherence to global best practices and reinforcing its commitment to prudent risk management.

- Integrating climate risk governance: The Bank is aligning with global standards by embedding climate risk governance, scoring, and data-driven disclosures into its Risk Management Framework. This initiative enhances the Bank’s resilience to climate related risks, ensures compliance with evolving regulatory requirements, and promotes long-term sustainable growth.

- Commitment to customer centricity: Comprehensive internal training and knowledge sharing programs were conducted for Branch Managers and Credit Analysts. These sessions covered credit risk analysis, ECL assessment of Individually Significant Customers (ISCs) and environmental and social considerations, equipping stakeholders with essential expertise.

- Strengthened credit risk review process: The Credit Risk Review (CRR) mechanism has been enhanced, resulting in improved identification of potential credit deteriorations and minimised delinquencies. This progress is driven by the expansion of the centralised online oversight system, which now encompasses additional lending units and provides the IRMD with a growing wealth of timely and actionable risk insights, strengthening operational efficiency and decision making.

- Expansion of ECL review practices: The IRMD has enhanced its independent review of ECL assessments for ISCs. This enhancement expands coverage to encompass all lending units within the Bank's domestic and Bangladesh operations. The expanded scope has resulted in demonstrably improved consistency and accuracy of ECL assessments, coupled with enhanced coordination with lending units.

- Revision of threshold limits: In light of improving economic conditions and a healthy portfolio, and with Board approval, the Bank has adjusted the threshold limits for credit proposals reviewed by the IRMD, coupled with differentiated threshold framework for credit proposals, predicated on validated internal credit risk rating models. This revision reflects the Bank's responsiveness to market dynamics and the commitment to achieve optimised resource allocation and enhanced operational efficiency. Critically, the IRMD maintains a strong focus on significant credit exposures, ensuring rigorous oversight even with adjusted thresholds.

- The Risk Elevated Industry (REI) assessment process: Encompassing both initial assessments and subsequent reviews for credit facility upgrades, has been centralised and entrusted to the IRMD. This centralisation enhances efficiency, eliminates operational burden from Lending Officers, and ensures improved accuracy, consistency, and expedited processing of these critical risk assessments.

- Integration of technology risk into Risk and Control Self Assessment (RCSA) Framework: Broadening its risk management scope, the IRMD has successfully integrated technology risk into the Risk Control Self-Assessment framework, enhancing the Bank's resilience to technological vulnerabilities.

- Pursuit of ISO 22301:2019 certification: To align with global best practices in Business Continuity and Disaster Recovery, the Bank has engaged external expertise to achieve ISO 22301:2019 certification. This underscores its commitment to operational excellence and organizational sustainability.

- Introduction of Technology Risk Framework and setting up steering committee: This is in tandem with the rapid embracing of new technologies into the Bank’s ecosystem as a balancing act that helps the Bank in managing the relatively new risk vistas it may get exposed in the new digital era.

- Strengthening Data Governance: Data Breach Handling Policy and Procedure were implemented to strengthen and enhance the Bank’s overall Data Governance Policy Framework, in accordance with the Personal Data Protection Act 09 of 2022.

Details of the specific activities undertaken by the Board Integrated Risk Management Committee (BIRMC) during the year to strengthen risk governance and management are given in its report on pages 218 and 220 of this Annual Report.

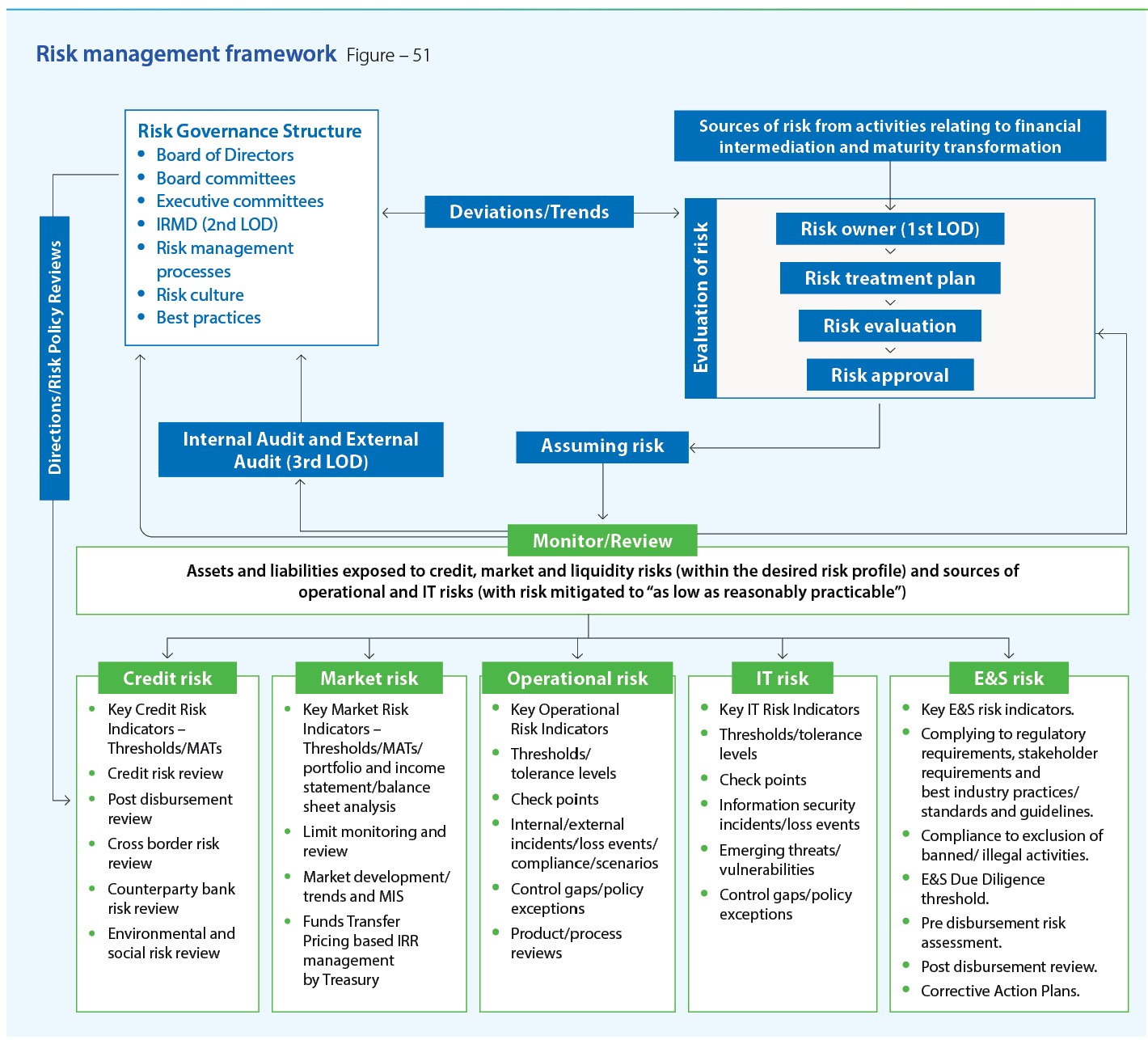

Risk Management Framework

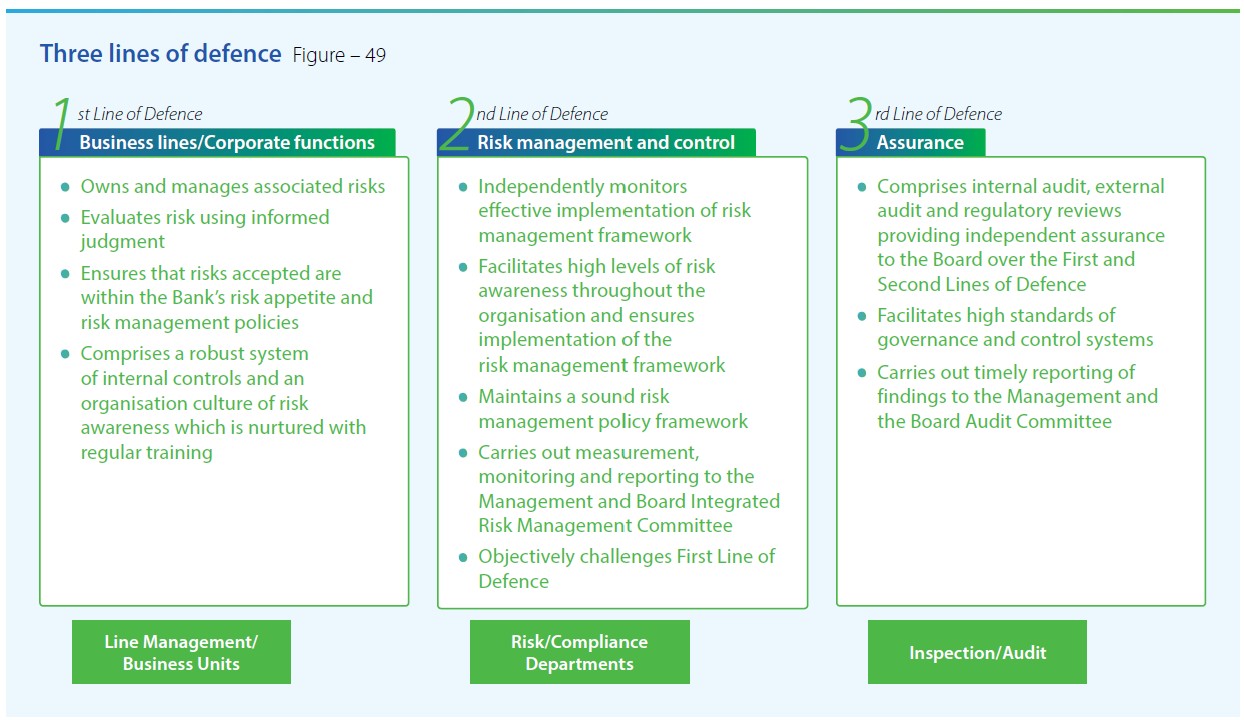

The Bank’s Integrated Risk Management Framework (IRMF) is a robust and comprehensive structure designed in accordance with CBSL guidelines and based on the internationally recognised Three Lines Model. This framework delineates the specific roles and responsibilities of various departments within the Bank, ensuring a coordinated and effective approach to managing risks.

The IRMF encompasses all risk exposures through a structured methodology supported by well-defined organisational structures, advanced systems, efficient processes, and globally benchmarked best practices. It provides a systematic approach to identifying, mitigating, and addressing potential risks, uncertainties, and losses faced by the Bank.

By adhering to the Three Lines model, the framework balances operational responsibilities while equipping the Bank with specialised skills and tools to manage risks effectively. The IRMF undergoes an annual review or is updated more frequently as needed to reflect changes in regulatory requirements, operational dynamics, and the evolving risk landscape.

Board of Directors

The Board of Directors functions as the highest governing authority, responsible for formulating the Bank’s strategies and policies, setting objectives, and overseeing executive operations. It holds the ultimate accountability for supervising the risks undertaken by the Bank and its Group entities, ensuring these are effectively identified and managed. (Refer for detailed profiles of the Board of Directors.)

The Board defines the Bank’s risk appetite by maintaining a balance between achieving strategic objectives and managing the risks associated with pursuing those objectives. Oversight responsibilities are delegated to various Board committees, listed on page 197, which are supported by executive-level counterparts. These committees work in close collaboration with the executive management to assess the effectiveness of the Bank’s risk management framework. They regularly report their findings to the Board, offering a comprehensive perspective on the Bank’s risk profile, management actions, and outcomes. This process enables the Board to identify risk exposures, address gaps, and implement mitigation measures in a timely manner.

The Board actively guides executive management to ensure that business strategies and objectives are aligned with the desired risk levels. The leadership and ethical tone set by the Board, combined with its strong corporate culture, are instrumental in managing risks effectively throughout the Bank.

In addition to adhering to the Three Lines Model, the Bank places a strong emphasis on ethical conduct as a core element of risk management. The Bank’s commitment to responsible, transparent, and disciplined business practices is clearly outlined in various policies and frameworks, including the Code of Ethics, Gift Policy, Communication Policy, Credit Policy, Anti-Bribery and Anti-Corruption Policy, and Conduct Risk Management Policy Framework. These documents set clear expectations for all employees to uphold the highest standards of honesty, integrity, and accountability.

The Board also ensures diligent oversight of the risk profiles of all subsidiaries within the Group, in addition to that of the Bank, recognising the potential financial and reputational risks involved. This oversight is conducted in strict compliance with regulatory requirements. (Refer Group structure for the list of subsidiaries.)

Board committees

The Board has established four dedicated committees to support its oversight responsibilities for risk management and to ensure the adequacy and effectiveness of the Bank’s internal control systems. These committees are:

- Board Audit Committee (BAC)

- Board Integrated Risk Management Committee (BIRMC)

- Board Credit Committee (BCC)

- Board Strategy Development Committee (BSDC)

Each committee functions under clearly defined Terms of Reference (ToR) and convenes meetings at predetermined intervals or as required. Through their discussions and evaluations, these committees provide recommendations to the Board on critical areas such as risk appetite, risk profile, strategy, risk management and internal control frameworks, risk policies, limits, and delegated authority.

For detailed information on the composition, Terms of Reference, authority, meeting schedules, attendance, activities undertaken during the year, and other relevant aspects, please refer to the respective committee reports.

Executive committees

The executive management is responsible for implementing strategies and plans as mandated by the Board of Directors while ensuring that the Bank’s risk profile remains within the approved risk appetite. The Executive Integrated Risk Management Committee (EIRMC), composed of members from units overseeing credit risk, market risk, liquidity risk, operational risk, and IT risk, leads this effort. To address specific risk areas comprehensively, the EIRMC is supported by several dedicated committees, facilitating effective risk management across both the First and Second Lines of Defence:

- Asset and Liability Management Committee (ALCO)

- Credit Policy Committee (CPC)

- Executive Committee on Monitoring Non-Performing Credit Facilities (ECMN)

- Information Security Council (ISC)

- Business Continuity Management Steering Committee (BCMSC)

- Executive Sustainability Committee (ESC)

- Recovery Plan Steering Committee (RPSC)

The EIRMC maintains active communication with the BIRMC to ensure that risk management activities align with the IRMF and that risks are managed within established parameters. The Chief Risk Officer (CRO) directly reports to the BIRMC, underscoring the independence of the risk management function. Details regarding the composition of the executive committees can be found in the “Annual Corporate Governance Report” on pages 201 and 203.

The CRO, who heads the IRMD, plays a pivotal role in ensuring risk governance by participating in major risk and control forums, including meetings of the BIRMC, BCC, and BAC. The IRMD is entrusted with independently monitoring the compliance of the First Line of Defence with established policies, procedures, guidelines, and limits. Any deviations are escalated to the relevant executive committees for further action.

Further, the IRMD provides a holistic view of all types of risk, enabling independent risk assessments by the executive committees. The findings and recommendations are shared with Line Managers and Senior Management, fostering effective communication, promoting discussions, and driving necessary actions to mitigate risks and enhance the Bank’s resilience.

Risk management

Risk management involves the critical responsibility of identifying, assessing, controlling, and mitigating risks. This includes developing and implementing risk mitigation strategies, monitoring Early Warning Signals (EWS), estimating potential future losses, and taking proactive measures to manage or transfer risks effectively. The Bank’s risk management framework (depicted in Figure 51) serves as a guide for designing and executing risk management strategies, policies, and procedures, ensuring alignment with the strategic priorities outlined in the Bank’s Corporate Plan and its defined risk appetite.

To enhance its risk detection and management capabilities, the Bank has made significant investments in developing a robust infrastructure. This infrastructure includes foundational resources such as policies, procedures, guidelines, circulars, limits, software platforms, risk assessment tools, databases, and expertise. Additionally, the Bank has implemented risk dashboards and predictive modeling capabilities to support real-time monitoring and decision-making. These elements are complemented by incident response mechanisms, advanced data analytics, and streamlined communication channels, all aligned with international best practices to ensure the effectiveness of risk management processes.

This infrastructure establishes the foundation for applying specific risk management tools, enabling the Bank to proactively identify, assess, and manage risks while ensuring regulatory compliance and operational resilience.

Recognising that risk management is a shared responsibility across the organisation, the Bank emphasises the importance of equipping all employees with a clear understanding of the risks they may encounter. The IRMD plays a key role in fostering a strong risk culture by providing continuous training and awareness programs. These initiatives focus particularly on risk owners, offering knowledge and skill-building opportunities to ensure that all employees are well-prepared to address risks effectively and contribute to the Bank’s overall resilience.

Policies, procedures, and limits

The Bank has implemented a comprehensive suite of risk management policies that address all managed risks, ensuring robust governance and regulatory compliance. These policies provide clear guidance to business and support units on managing risks effectively and adhering to regulatory requirements, including the Banking Act Direction No. 07 of 2011 – Integrated Risk Management Framework for Licensed Commercial Banks, developed in alignment with the Basel Framework, as well as subsequent directives issued by the CBSL.

By institutionalising a structured knowledge base, these policies aim to minimise bias and subjectivity in risk-related decision-making. Core documents, such as risk management policies, play a critical role in shaping the Bank’s risk culture by clearly defining objectives, priorities, processes, and the roles and responsibilities of the Board of Directors and the Management in risk governance.

The Risk Appetite Statement (RAS) is a key element of the Bank’s risk management framework, establishing the limits within which risks must be managed. The RAS is reviewed and updated by the BIRMC and the Board of Directors at least annually or more frequently, in line with evolving regulatory and business requirements.

To ensure the Bank’s overall risk exposure, including that of its international operations, aligns with CBSL’s regulatory framework, the Bank considers the regulatory landscapes in all jurisdictions where it operates. Operational guidelines are issued to facilitate the implementation of the Risk Management Policy and ensure compliance with the limits outlined in the RAS. These guidelines provide employees with detailed instructions on the types of facilities, processes, and terms and conditions that govern the Bank’s daily operations.

Risk management tools

Building on its comprehensive infrastructure, the Bank employs a diverse range of qualitative and quantitative tools to identify, measure, manage, and report risks effectively. These tools are tailored to address specific risks based on factors such as the likelihood of occurrence, potential impact, and data availability.

Key tools utilised by the Bank include EWS, threat analysis, risk policies, risk registers, risk maps, and RCSA. These tools are complemented by advanced frameworks like the ICAAP, workflow-based operational risk management systems, and the Environmental and Social Management System (ESMS).

To enhance risk quantification and mitigation, the Bank employs diversification strategies, insurance, benchmarking, gap analysis, and Net Present Value (NPV) analysis. Additionally, advanced products such as SWAPs, Caps and Floors, hedging and techniques like risk scoring, stress-testing, duration analysis, Value at Risk (VaR) assessments , and scenario analysis are integral to managing market and credit risks.

These tools and techniques collectively ensure that risks across all dimensions of the Bank’s operations are managed effectively within the parameters of its risk appetite and governance frameworks.

Sustainability and Climate Risk

Sustainability and climate-related risks, including Environmental and Social (E&S) risks, are pivotal components of the Bank's risk management strategy. These risks stem from a wide range of ESG factors that directly or indirectly influence the Bank’s operations, lending activities, reputation, and long-term viability. By addressing these interconnected risks, the Bank reinforces its commitment to responsible banking and positions itself as a leader in sustainable development.

The Bank recognises that sustainability risks not only pose challenges but also provide opportunities for innovation, growth, and resilience. Incorporating ESG considerations into decision-making and operational practices strengthens the Bank's ability to create value for all stakeholders while aligning with global sustainability goals, such as the United Nations’ Sustainable Development Goals (SDGs) and the Paris Agreement.

Key risk areas

The Bank has categorised sustainability and climate-related risks into three primary domains to ensure comprehensive identification and management:

Environmental risks

- Climate-related risks:

- Physical risks:

- Transition risks

- Resource depletion and biodiversity loss

- Pollution including air, water, soil contamination, and greenhouse gas emissions

– Acute events such as floods, hurricanes, and droughts

– Chronic changes such as rising sea levels, temperature variations, and shifting rainfall patterns

– Impact on assets, infrastructure, and supply chains, affecting borrowers’ financial stability and the Bank's operational continuity

– Policy changes such as carbon taxes, emission reduction targets, and environmental regulations

– Market dynamics, including shifts in consumer preferences towards sustainable products and technologies

– Reputational risks linked to perceived inaction on climate change the Bank and/or borrowers

Social risks

- Unfair labour practices, including forced and child labour

- Occupational health and safety hazards

- Community displacement and cultural heritage loss due to project financing

- Discrimination, lack of diversity, and inequitable access to resources

- Reputational risks arising from borrower practices that fail to meet ethical or social expectations

Governance risks

- Bribery and corruption, unethical business conduct, and financial crimes

- Information security breaches and inadequate IT governance

- Poor compliance with international frameworks and regulatory standards

Integrated framework for sustainability and climate risk management

The Bank’s approach to managing these risks is guided by its comprehensive Sustainability Framework. This framework aligns with international best practices, including the IFC Performance Standards and the SLFRS S1 & S2. Supporting systems and policies include:

- A systematic mechanism to assess and mitigate E&S risks across lending activities, operations, and stakeholder engagements

- Incorporates tools for identifying and addressing potential risks at every stage of the project lifecycle

- Outlines principles for sustainable development, including environmental protection, social equity, and ethical governance

- Defines risk assessment processes, mitigation measures, and criteria for excluded activities

- Aims to systematically identify, assess, and manage climate-related risks at both the portfolio and project levels

- Emphasises integrating climate considerations into existing risk management processes

1. Environmental and Social Management System (ESMS):

1.1 Environmental and Social Risk Management Policy:

1.2 Environmental and Social Risk Assessment and Management Procedure:

Defines risk assessment and management processes: criteria for excluded activities, environmental and social risks screening, pre-defined thresholds for due diligence, mitigation measures/corrective action plans for material risks, and process for monitoring compliance to corrective actions.

2. Climate Risk Management Framework (to be implemented in 2025)

Impact of sustainability and climate-related risks

The Bank acknowledges that inadequate management of these risks could result in:

- Financial impacts: Loan defaults, increased credit risk, asset devaluation, and higher operational costs due to climate-related disruptions.

- Reputational damage: Loss of stakeholder trust due to perceived inaction or association with unsustainable practices.

- Legal and regulatory consequences: Penalties, lawsuits, or enforcement actions resulting from non-compliance with sustainability-related regulations.

List of climate related risks is given in the Tables 58 and 59 on pages 276 and 277 and the climate related opportunities in the Table 60 on page 278.

**In line with the requirements specified under SLFRS S2, a preliminarily level assessment has been carried out by the Bank. However, this assessment will be further improved through the Bank’s continuous commitment by investing on climate data capabilities and climate risk management.

- Climate-related risks:

Climate change can have widespread and significant impacts across sectors and geographies, potentially affecting the financial system. The identified climate related risks are categorised into three different time buckets in line with their synchronisation with the Bank’s financial and capital budgets, as listed below:

- Short term (ST): 0-1 year

- Medium term (MT): 1-5 years

- Long term (LT): 5-30 years

As the crystallisation of climate related risks of the Bank’s portfolios, through macro and micro transmission channels, emerged through traditional risk categories such as credit risk, market risk, operational risk and reputational risk etc., Climate risk itself is treated as a risk driver.

Climate related Physical Risks Table – 58

| Category | Climate Related Risk driver |

Time Horizon | Impact on Business Model |

Direct/ Indirect Impact |

Principal Risk category to the Bank |

Strategy & Decisions (adaptation/mitigation) |

| Acute | Extreme weather events (floods, storms, landslides) | ST, MT | Disruption of business operations of the Bank Infrastructure damage, service disruptions, Decreasing Supplies, increased operational costs, Adaptation costs |

Direct | Operational Risk, Reputation Risk | Disaster preparedness, Business Continuity planning, budget allocations for repair work and structural reinforcements, Digital Transformation to Remote Services -enhancing digital banking services to ensure customers can access banking services even during physical disruptions. |

| ST, MT | Disruption Borrowers’ business operations Infrastructure damage, service disruptions, Decreasing Supplies, increased operational costs, Adaptation costs leading to Increased loan defaults, collateral devaluation | Indirect | Credit Risk | Incorporating physical climate risks into the credit evaluations, insurance coverage, Diversify the loan portfolio across different sectors and geographic areas, | ||

| Chronic | Sea-level rise | LT | Damage to business premises in coastal belt | Direct | Operational Risk Reputation Risk | budget allocations for structural reinforcements, Relocation plans, |

| LT | Damage to borrower’s business premises in coastal belt | Indirect | Credit Risk, Operational Risk | Regularly assess and adjust the loan and investment portfolio to minimise exposure to sectors vulnerable to climate impacts | ||

| Rising temperatures |

MT, LT | Business disruptions, Heat waves can strain cooling systems for data centers, increasing the risk of outages or data loss, affect human health, leading to heat-related illnesses, Reduce labour productivity | Indirect | Operational Risk Reputation Risk, | budget allocations for backup systems, Business Continuity plans, employee support programs |

Climate related Transition Risks Table – 59

| Climate Transition risk driver |

Description | Time Horizon |

Impact on Business Model |

Direct/Indirect Impact |

Principal Risk | Strategy & Decision Making |

| Policy & Legal | Requirement of de-carbonization of loan portfolio |

MT, LT | Loss of revenue from clients with high carbon intensity | Direct | Strategic Risk | Green financing, loan tenure adjustments, Support customers in their transition to a net zero economy, |

| Absence of carbon pricing policies | MT | Missed innovation opportunities | Direct | Strategic Risk | Alignment with national policies and climate strategies and Nationally Determined Contributions (NDC) | |

| EU Carbon Border Adjustment Mechanism (CBAM) | MT, LT | Increased credit risk for export clients |

Indirect | Credit Risk | Transitional finance, climate stress-testing | |

| Reputation | Bank’s reputation affected by slow transition | MT, LT | investor concerns, Loss of customers | Direct | Reputational Risk | Proactive climate strategies, scenario planning, report on progress in supporting the green transition to Bank’s stakeholders |

| Funding clients slow to adapt |

MT, LT | Higher costs, slow adoption of sustainable processors | Direct | Credit Risk Market Risk Reputational Risk | Climate-focused lending policies, ESG alignment, Build resilience by embedding climate risk impacts in decision making processes | |

| Market | Shifts in consumer preferences toward sustainable technologies | MT, LT | Impact industries dependent on traditional, carbon-intensive technologies, Market share loss to competitors, may result in stranded assets, Decline in equity prices of carbon-intensive firms | Direct | Credit risk Market Risk | Digital transformation, sustainable banking products Diversification, green investments, Monitoring macroeconomic conditions, strategic alignment |

Climate related Opportunities Table – 60

| Category | Opportunity Description | Time Horizon | Business Impact | Strategy & Decision Making |

| Working towards making the Bank operations Net zero aligning with country plans and targets | Energy efficiency & resource optimization | ST, MT, LT | Cost reduction, improved efficiency, Reduced carbon footprint, National policy alignment and regulatory compliance, | Incentives for energy-saving innovations, employee KPIs linked to reducing carbon footprint |

| Renewable energy transition | ST, MT, LT | Renewable installations targets, investing in carbon credit schemes | ||

| Financing to Sustainable businesses and Circular Economy | ST, MT, LT | Market expansion, enhanced ESG profile with market reputation, National policy and NDC alignment and regulatory compliance Positive Impact on market share of the Bank. | Targets in corporate plan, Green financing targets(financing to the activities eligible under the climate mitigation criteria given in Green Finance Taxonomy of Sri Lanka) , digital banking expansion | |

| Bank investments for Enhancing climate adaptive capacity and resilience of communities and ecosystems. | Financing to climate adaptation projects and companies engaged in climate resilience | ST, MT, LT | Market expansion, align with country's National Adaptation Plan (NAP) for Climate Change Impacts, Positive Impact on market share of the Bank. | Targets in corporate plan, Green financing targets(financing to the activities eligible under the climate adaptation criteria given in Green Finance Taxonomy of Sri Lanka) |

There will be opportunities available for the Bank, arising from the global transition to a low-carbon economy, which will involve scaling up zero or near-zero emitting technologies and supporting emissions reductions in high-emitting and hard-to-abate sectors, amid the global journey to minimise the worst effects of climate change.

Banks have several opportunities due to climate adaptation, ranging from financial products to risk management strategies. Climate adaptation finance is becoming a growing market, especially as businesses and governments invest in resilience against physical climate risks.

Proactive risk management measures related to ESCR

The Bank employs a multi-faceted approach to manage sustainability and climate-related risks effectively:

- Comprehensive due diligence for all lending activities, incorporating ESG and climate risk evaluations.

- Detailed climate risk assessments, including the identification of physical and transition risks, supported by scenario analysis and stress-testing.

- Use of internationally recognised metrics such as Scope 1, Scope 2, and if applicable, Scope 3 greenhouse gas emissions to quantify climate-related impacts.

- Avoiding financing for activities deemed illegal or unsustainable, such as projects involving unsustainable resource extraction/utilization, forced labour, destruction of critical habitats, destruction of cultural heritage or trade in banned substances.

- Partnering with borrowers to improve their ESG practices through capacity building, technical assistance, and alignment with global standards.

- Strengthening the Bank’s internal operations to reflect its sustainability values, including adopting energy-efficient technologies and reducing its carbon footprint.

- Regular monitoring of borrower compliance with E&S requirements, supported by annual performance reviews and real-time tracking tools.

- Quarterly reporting of climate and E&S risk metrics to the Board and management committees, ensuring transparency and accountability.

- Use of risk dashboards to visualise and analyse the Bank’s overall risk exposure across products, portfolios, and geographies.

- Active oversight by the Board of Directors, ensuring alignment with regulatory standards and international best practices.

- Integration of climate considerations into governance structures such as the EIRMC and the BIRMC.

- Establishment of a Climate Risk Workgroup to drive the development and implementation of climate strategies.

1. Risk identification and assessment:

2. Risk mitigation:

3. Monitoring and reporting:

4. Governance and oversight:

During the year 2024, the E&S risk screening outcome is given in Graph 59.

Environmental and social risk category wise distribution of lending proposals as at December 31, 2024 Graph – 59

|

Category A – Projects with High environmental and/or social risks. |

|

Category B – Projects with Medium environmental and/or social risks |

|

Category C – Projects with Low environmental and/or social risks projects |

-DP_Edited-web-resources/image/619.png)